A Brief History of Prop 2½

By Ellen Putnam

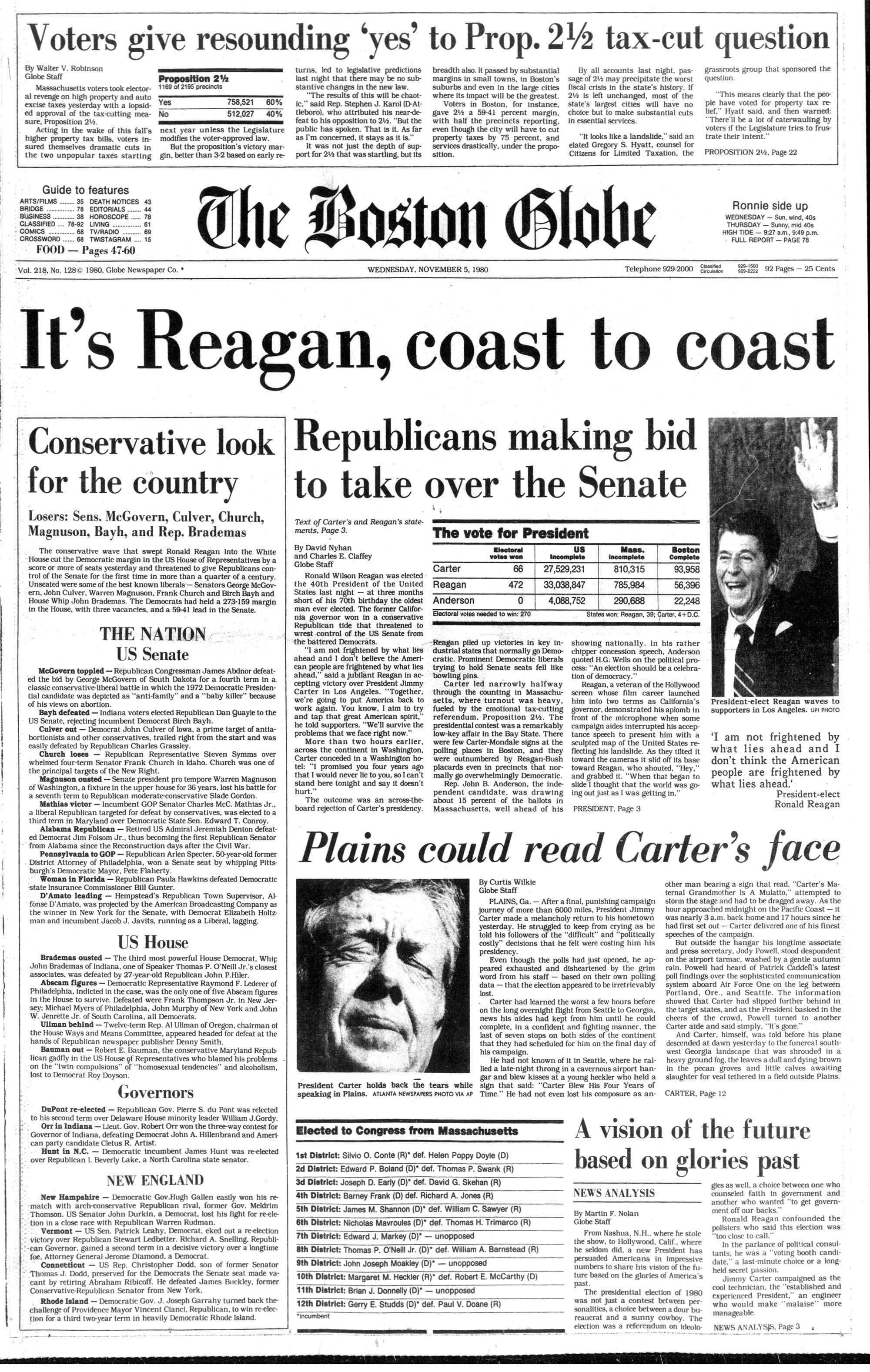

Front Page of The Boston Globe, November 5th, 1980

From The Boston Globe

In 1980, Massachusetts voters approved a statewide ballot initiative called Proposition 2½ (Prop 2½). This law has profoundly affected municipal finances in the 45 years since then. And it is a subject of particular interest in Melrose right now as the city prepares to vote on a Proposition 2½ override in November’s municipal election.

But what is Prop 2½, and what are its implications for Melrose?

Prior to Prop 2½, the tax structure in Massachusetts was much more heavily weighted toward property taxes than most other states were. In 1977, property taxes made up almost 50% of all state and local taxes in Massachusetts, compared to the national average of 35%. And this had been a problem for some time: 35 years before the ballot measure, in 1945, the Legislature’s Special Commission on Real Estate concluded that real estate was “grossly, even dangerously overtaxed.”

But attempts at legislation to rebalance the tax system all failed - until voters passed Prop 2½ in 1980.

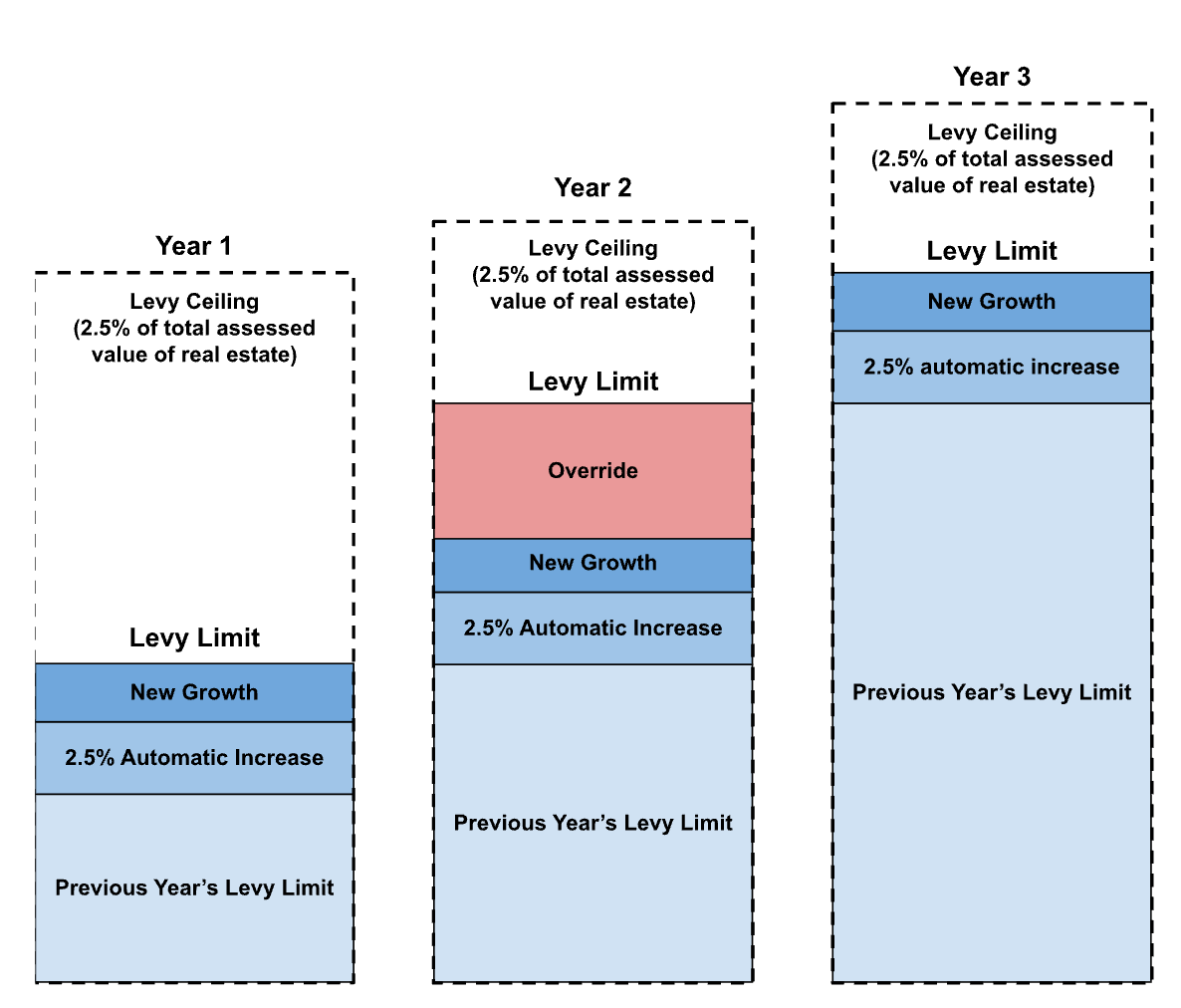

Prop 2½ has two main aspects: the levy ceiling and the levy limit.

The levy ceiling prevents cities and towns from taxing above 2.5% of the assessed value of all real estate in the town. Under the law, the amount a city or town collects in property taxes can never exceed the levy ceiling.

In the early days of Prop 2½, some cities, including Cambridge and Boston, actually had to step down their property taxes over several years to meet the levy ceiling. More recently, some towns in Western Massachusetts are having financial difficulties because they cannot further increase their property tax levy due to the levy ceiling.

The main challenge for municipal budgets in Melrose and other communities like us, however, comes from the other aspect of the law: the levy limit.

The levy limit is the maximum a city or town can collect in property taxes each year - and it is not permitted to exceed the levy ceiling. The levy limit restricts cities and towns from increasing the total amount of property taxes collected by more than 2.5% each year, plus some amount calculated to reflect new growth in the town.

New growth includes the construction of new housing and the accompanying population growth, but it does not take into account rising property values. In Melrose, the tax rate (the amount the owner pays in taxes per $1,000 of their property’s assessed value) has actually decreased in recent years, even as property values have increased - and as the amount that the average family pays in property taxes has also gone up.

Cities and towns in Massachusetts are limited in the types of taxes they can levy: property taxes, local meals and lodgings tax, vehicle excise taxes, and a variety of user fees. And for most cities and towns, none of those other sources of revenue generate anywhere close to the amount that property taxes do.

When Prop 2½ passed, inflation rates were at almost 14%, and they have never been as high since. But in years when inflation is higher than 2.5% - as it has been since 2021 - or when specific costs, such as health insurance premiums or special education costs, rise faster than 2.5%, the city is faced with having to cut services in order to make up the deficit.

Illustration of how an override affects levy limits under Prop 2½

(Not even remotely to scale)

Prop 2½ includes a provision that allows cities and towns to call for an override vote, where voters can choose to raise the levy limit by a certain amount in one year, which then is used to calculate the levy limit for the following year. There are no restrictions in the law on how much municipal leaders can ask for in an override vote or how often votes can be called - however, voters need to approve an override (with more “Yes” votes than “No” votes) in order for it to go into effect.

Speaking about Prop 2½ in 2014 (in a Boston Globe article that also includes perspectives from then-Mayor of Melrose Rob Dolan), Barbara Anderson, the executive director of Citizens for Limited Taxation and the driving force behind the 1980 ballot initiative, reflected, “Prop 2½ allows overrides and debt exclusions, if local voters can be convinced to approve them. When local officials want more money than the levy limit allows, they must ask for it, instead of just taking it as they did before 1980. Citizen empowerment is one of the best things about our property tax limit.”

The Institute on Taxation and Economic Policy, a nonpartisan nonprofit that looks at taxation around the country, notes that Prop 2½ led to changes in the way Massachusetts funds its local governments and school systems.

“Though the policies were generally portrayed as a tax cut,” the Institute explained, “they were not framed to voters as a hit to municipal financial stability. Some voters might not have understood that these limits would cut local government funding or might not have grasped the degree to which that would happen or how it might affect their cities or schools. The erosion of local government authority over their own tax bases has had massive implications for how local governments and state governments interact.”

WGBH’s Scratch & Win podcast described the success and the consequences of Proposition 2½, which won by “decoupling the question of taxes from the question of spending,” according to Isaac Martin, Professor of Urban Studies and Planning at the University of California San Diego. “Ask people, ‘Hey, do you want lower taxes?’ And don’t tell them what it would cost them in terms of lost public services. And that could become a winning election issue.”

Prior to the passage of Prop 2½, state aid for cities and towns was largely an afterthought; now, with local funding limited, municipal governments rely more heavily on state aid.

“In Massachusetts, Proposition 2½ has unintentionally led to differential school spending results based on how high the property values are,” the Institute on Taxation and Economic Policy went on. “In lower-income areas, the state spends more money per pupil to make up for the lack of property tax revenues. In higher-income areas, voters can override the cap and can cover the per-pupil spending themselves. However, middle-income districts are often squeezed. While they frequently have levels of per-pupil spending that are adequate for the state, they receive no extra benefit, nor are residents willing or able to spend more, meaning those school districts are stuck with fewer resources.”

There has been some discussion since 1980 of whether the state legislature could update or repeal Proposition 2½.

Speaking to the City Council and the School Committee earlier this month, State Representative Lipper-Garabedian noted that one option would be to tie the property tax growth limits under Proposition 2½ to inflation. But she cautioned that colleagues have told her, “If we do that in the Legislature, there will be a ballot initiative the next day to repeal what we have done.”

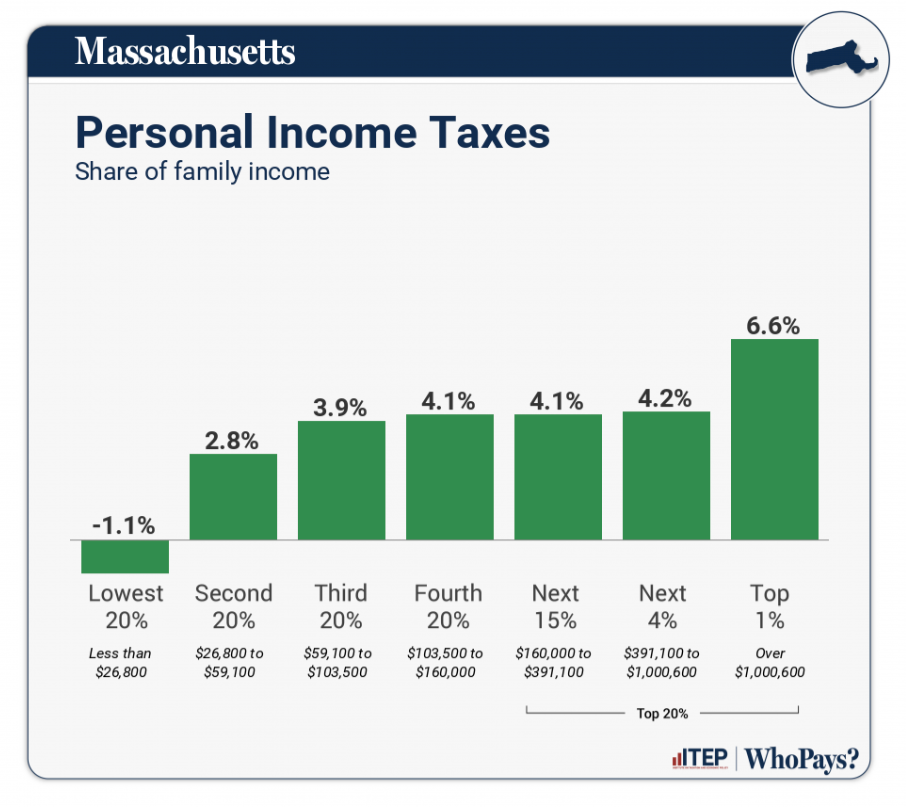

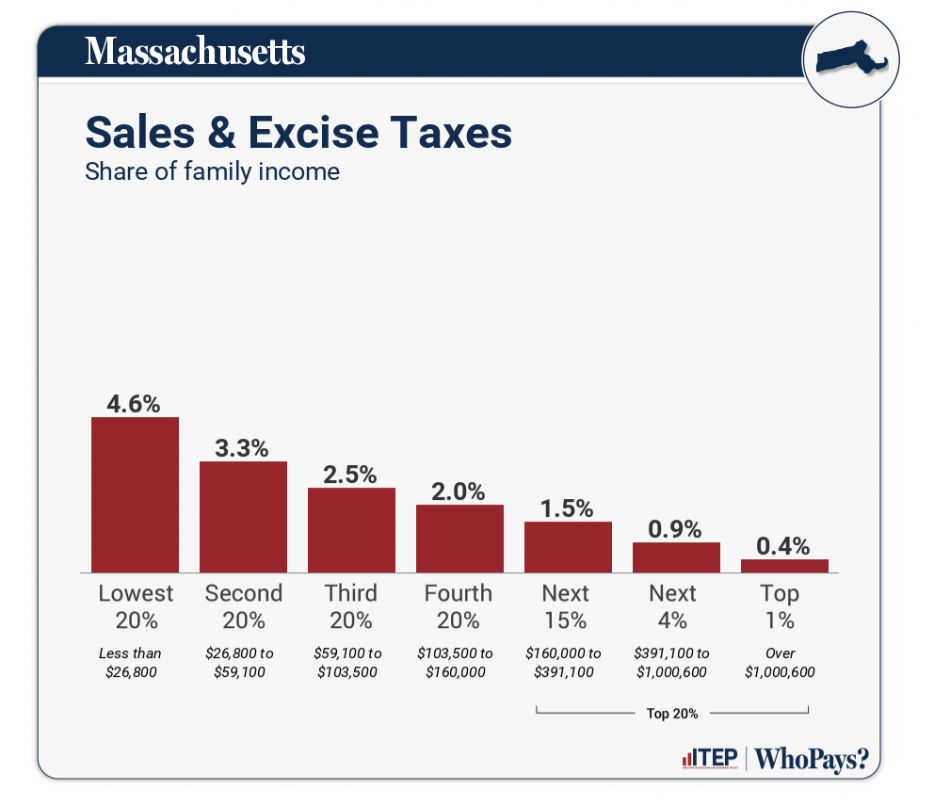

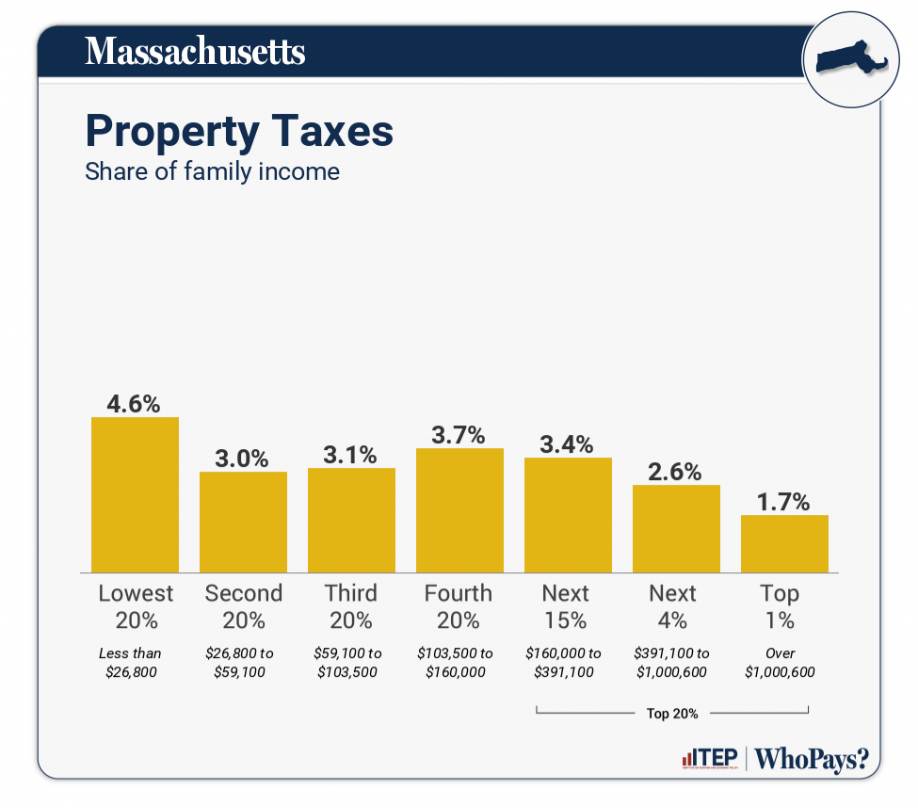

The Institute on Taxation and Economic Policy notes that, while the tax system in Massachusetts is fairly progressive relative to other states (meaning that higher-income families pay a higher percentage of their income in taxes than lower-income families do), the state’s comparatively high reliance on property taxes still makes the tax system more regressive than it could be.

Income taxes are generally progressive, meaning that higher-income families pay a higher percentage of their income than lower-income families do.

Sales taxes tend to be very regressive, because lower-income families genereally spend a higher percentage of their income on goods and necessities than higher-income families do.

Property taxes are fairly regressive, because higher-income families tend to have a lower percentage of their family’s wealth invested in property than lower-income families do, even if their property is worth more.

Interestingly, the Institute on Taxation and Economic Policy argues that property tax limits like Prop 2½ have not actually achieved their goal of making the tax system more equitable. They suggest that states can make their property tax structures less regressive by instead:

- Passing property tax circuit breakers for low-income homeowners and renters - (Massachusetts currently offers a senior circuit breaker, but the state circuit breaker program offers no relief for those younger than 65)

- Allowing for local income taxes - (This is currently not permitted under the state tax structure, and would require a change in state law)

- Equalizing school funding formulas - (Changing our school funding formulas would be a challenge without a significant increase in state revenue, because no state representative or senator would vote to decrease the amount of state aid that goes to their district)

All of these options would require new state laws, some of them extensive - and none would be likely to go into effect before Melrose sets its budget for Fiscal Year 2027 next spring.